Importing Wine in the EU: Excise Duty & EMCS Explained

If you buy Italian wine wholesale from another EU country, excise duty works differently from VAT — and getting it wrong is expensive. This guide explains excise duty on wine, the EMCS and the electronic Administrative Document (e-AD), and who pays what, where, so B2B buyers know exactly how a duty-suspended wine movement reaches them.

This guide is general information, not legal or tax advice. Excise rates and procedures change and vary by country. Always confirm current requirements with the relevant tax authority and your own advisor.

What is excise duty on wine?

Excise duty is a consumption tax levied on specific goods — alcohol, tobacco and energy products — separately from and in addition to VAT. Wine is an excise good under EU law: still wine, sparkling wine and intermediate products are all defined and classified in Council Directive 92/83/EEC on the structures of excise duties on alcohol and alcoholic beverages. The duty on wine is calculated per hectolitre of finished product, not on its value. Because excise is a separate tax, a shipment of Italian wine can cross the EU with 0% VAT under the reverse charge and still trigger an excise obligation.

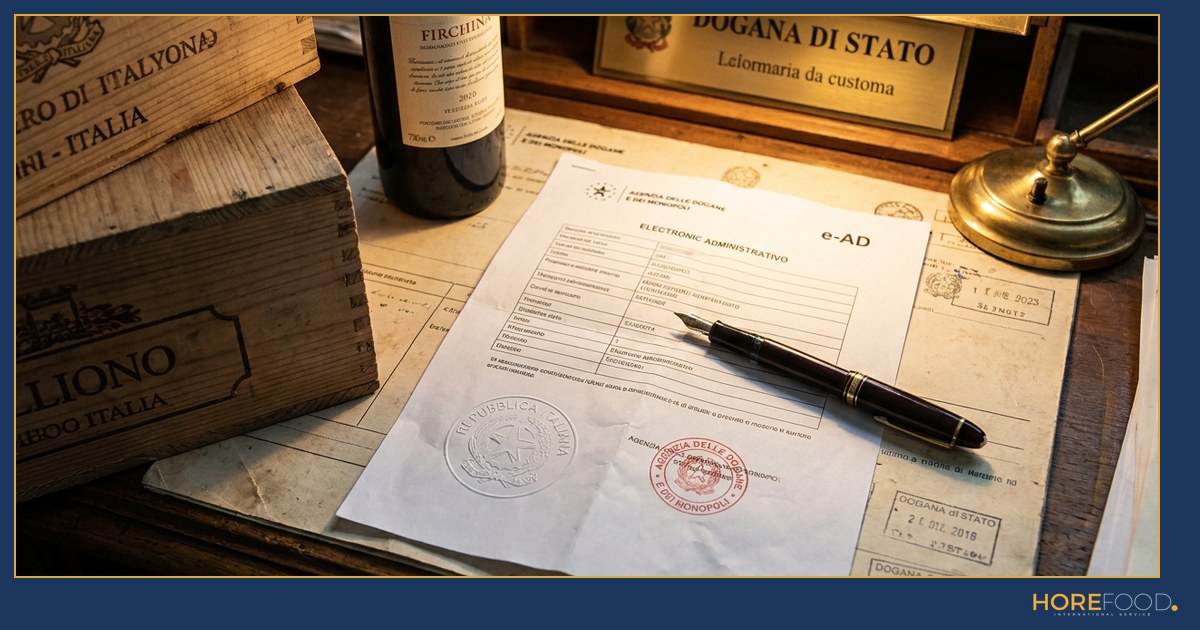

What is the EMCS and the e-AD?

The EMCS (Excise Movement and Control System) is the EU’s computerised system for recording and monitoring movements of excise goods across member states. When wine moves under duty suspension, every stage is documented electronically through an e-AD (electronic Administrative Document). The e-AD carries a unique Administrative Reference Code (ARC) that follows the consignment from dispatch to receipt. According to the European Commission, more than 190,000 economic operators use the EMCS, and since Phase 4.0 (in force 13 February 2023) commercial excise movements across the EU are fully paperless.

How does duty suspension work?

Duty suspension is a regime in which excise goods are produced, held and moved with the excise duty not yet paid. Under Council Directive (EU) 2020/262 (the general arrangements for excise duty), duty-suspended goods move between authorised tax warehouses, dispatched by a registered consignor and received by a registered consignee, all tracked through the EMCS with an e-AD. The tax is only suspended, not cancelled — it becomes due later. This is what lets a pallet of wine leave an Italian tax warehouse and travel across the EU without duty being paid up front.

- Goods are dispatched from an authorised tax warehouse under an e-AD.

- The movement is tracked in the EMCS via its Administrative Reference Code.

- The consignee confirms receipt with a report of receipt, closing the e-AD.

- Excise becomes chargeable when the wine is released for consumption.

Who pays excise duty, and where?

Excise duty is due in the country of consumption, at that country’s national rate, when the goods are released for consumption there. Under Directive (EU) 2020/262, excise becomes chargeable at the time, and in the member state, where the wine leaves duty suspension. In practice this means the buyer’s country and the buyer’s setup determine the liability: if you receive duty-suspended wine, you generally need to be an authorised warehousekeeper or registered consignee, or use one, and account for the excise on release. If wine has already been released for consumption in one country and is then moved commercially to another, the duty is due again in the destination — handled via a registered consignor and consignee under the EMCS.

Do all EU countries charge excise on wine?

No — national rates on still wine vary widely, and several countries set them at zero. The EU minimum rate for still wine is EUR 0 per hectolitre, so member states are free to charge nothing or a substantial amount. Italy and Germany apply a zero rate on still wine; the Netherlands, by contrast, applies a positive rate (for example, per the national schedule, in the range of roughly EUR 48–96 per hectolitre depending on strength). This is why the destination matters: the same pallet carries no excise cost in one market and a real one in another.

How is this different from VAT?

VAT and excise are two separate taxes that apply at the same time but follow different rules. VAT on an intra-EU B2B sale is handled through the reverse charge under Article 196 of the VAT Directive 2006/112/EC — your supplier invoices at 0% and you account for VAT in your own country. Excise is not affected by the reverse charge: it is a physical-goods tax tied to the movement and release of the wine, tracked through the EMCS, and due in the country of consumption regardless of the VAT treatment. See our guide on EU reverse-charge VAT for Italian food for the VAT side, and importing Italian food into the EU for the wider intra-community picture.

How Horefood helps

Horefood is an Italian food and beverage wholesaler — a trade name of Horecarte B.V. (KvK 69696985, BTW NL857972145B01), Reeuwijk, Netherlands. For wine and spirits in our catalogue, we move the goods under duty suspension through the EMCS with an e-AD, dispatched from an authorised tax warehouse in Italy, so the consignment is documented correctly at the Italian end. We ship by the box, layer or pallet across the EU, and invoice intra-community sales at 0% under the Article 196 reverse charge to buyers with a valid VIES VAT number. Because excise is due in your country of consumption at your national rate, we help you understand what applies before you order — and if you want to match wines to their appellations, see our note on Italian wine classification (DOCG, DOC, IGT).

Open your B2B account · browse Italian wines · talk to our team about a duty-suspended wine order.